Forget Tesla’s production

hell. The hardest bit of EVs is the powering up

Car-buyers are getting behind the wheel of an electric vehicle (ev) in ever greater numbers. As battery costs tumble, prices are falling. Compared with internal combustion engine (ice) cars, which can be a pain to drive and service, electric cars are a thrillseeking motorist’s dream. But the shift to evs is about more than driving pleasure. Transport accounts for around a quarter of the world’s carbon emissions, and road vehicles for around three-quarters of that share. If the world is to have any chance of reaching net-zero by 2050, evs will need to take over, and soon.

The 6m pioneers who opt for evs this year will still represent only 8% of all car purchasers. That figure must rise to two-thirds by 2030 and to 100% by 2050. Many investors are operating on the assumption that this will all happen as smoothly as a Tesla accelerates. The soaring market values of Elon Musk’s $1trn company, newcomers such as Rivian, which makes electric pickup trucks, and Chinese luxury ev firms, attest to sky-high confidence. Electric-battery makers, too, are booming.

Look beyond the glamorous, high-tech-filled automobiles that most obviously embody the ev revolution, however, and a merciless bottleneck appears. Not even those eyeing a new ev are sufficiently aware of it. Governments are only waking up to the problem. Put simply: how will all the electric cars get charged?

The current number of public chargers—1.3m—cannot begin to satisfy the demands of the world’s rapidly expanding electric fleet. According to an estimate by the International Energy Agency (iea), a forecaster, by the end of this decade 40m public charging points will be needed, requiring an annual investment of $90bn a year as 2030 approaches. If net-zero goals are to be met, by 2050 the world will need five times as many.

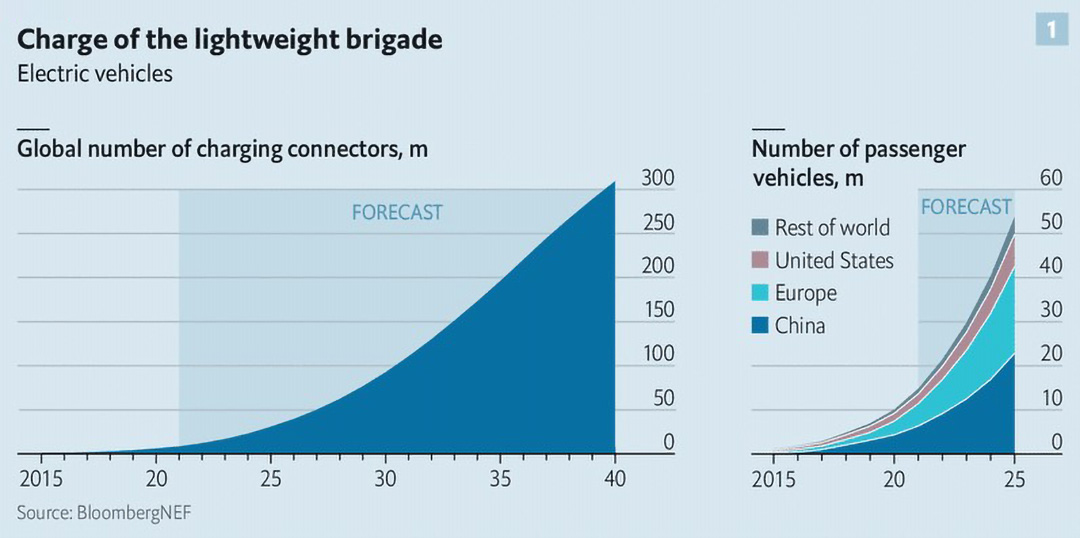

Governments’ current pledges to phase out ice cars and shift to evs are, it is true, not quite consistent with net-zero. Even if roads turn electric less speedily than they should, though, the sums the world needs to spend on charging infrastructure are still stupendous. In a slower scenario envisaged by Bloombergnef (bnef), a research firm, in which ev sales keep rising as battery prices fall but reach just under a third of all vehicles sold by 2030, roughly $600bn of investment would still be needed by 2040. That would pay for fewer chargers than the iea foresees—24m public points alone by 2040 (and 309m in total, see chart 1). If net-zero is to be achieved by 2050, bnef puts the cumulative charging investment required at a whopping $1.6trn.

Besides installing too few public chargers, the charging industry’s operational record is poor. The official number currently exceeds what some authorities reckon is needed. The European Commission, for example, thinks every ten evs require one public charger. According to the Boston Consulting Group (bcg), there are now five evs per charging point in the eu and China, and nine in America.

That is in theory. In practice, a survey of chargers in China by Volkswagen (vw) found many inoperable or “ iced” chargers (those blocked inadvertently or deliberately by fossil-fuelled cars). Only 30-40% of China’s 1m public points were available at any time. It is safe to assume some inoperability in the eu and America. This summer Herbert Diess, vw’s boss, complained on LinkedIn, a social network, that his holiday had gone less than smoothly because Ionity, a European charging network, provided too few points on the Brenner Pass between Austria and Italy. “Anything but a premium charging experience,” Mr Diess wrote. That vw part-owns Ionity made the criticism sting more.

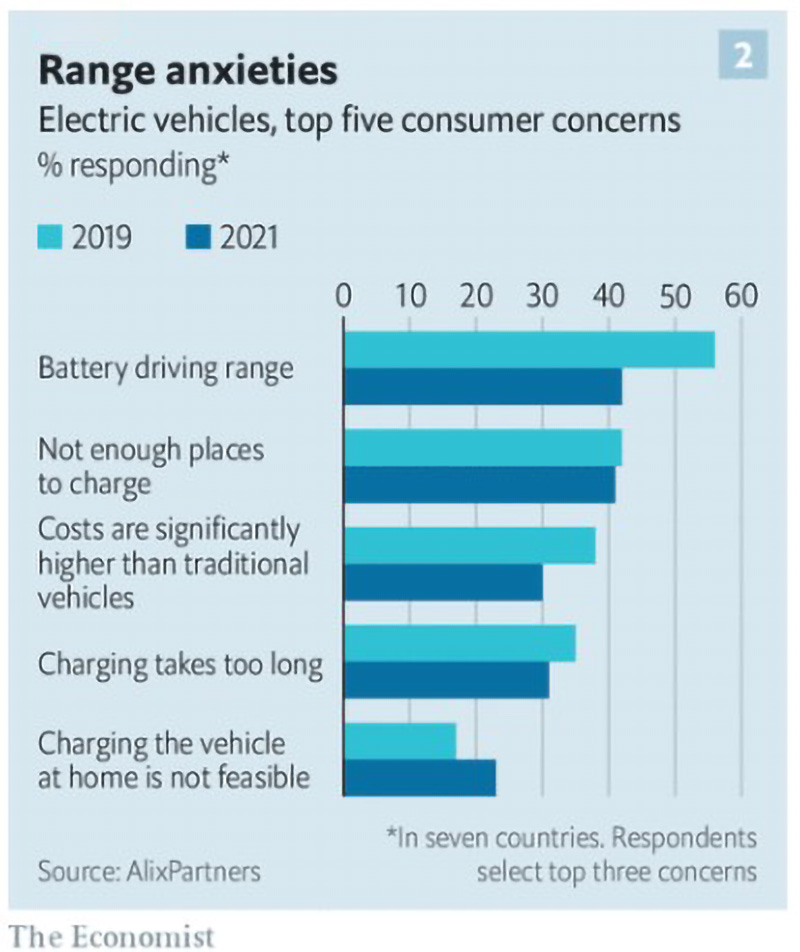

Drivers can smell trouble ahead. Range anxiety and the availability of public charging is a huge issue (see chart 2). In a recent survey by AlixPartners, a consultancy, in the seven countries that make up 85% of global ev sales the cars’ high prices came third on the list of top five reasons not to switch to battery power; the four others were all worries related to charging.

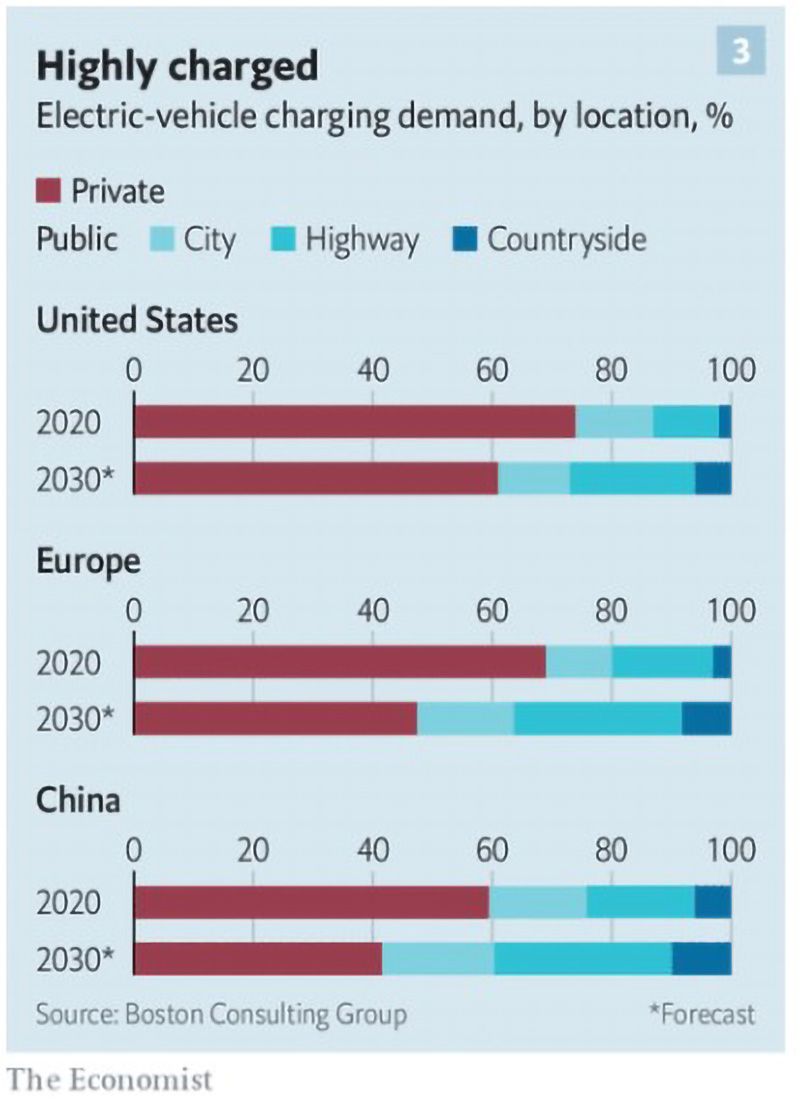

To assess the scale of the challenge start with the basics. A big advantage of evs is that they can be charged at home—or at workplaces, if employers install chargers. In America 70% of homes have off-street parking where a charger can be installed (the equivalent figure is lower in Europe and China). bcg estimates that in 2020 home and workplace charging accounted for nearly three-quarters of the total charging energy use in America, seven-tenths in Europe and three-fifths in China.

Current ev models typically have batteries with ranges of around 400km. Some go over 650km. The average American drives 50km a day, according to Bank of America. Europeans and Chinese drive less. Two types of charger are good enough to top up vehicles, or give them a boost overnight at home or during the working day. The slowest, providing up to 8km of range an hour, can do the job. So do “level 2” chargers that provide 16-32km. Both are easy on the wallet. Drivers can use dedicated sockets that cost a few hundred dollars (and are often subsidised by governments) to tap the cheapest electricity tariffs.

Nonetheless, home and workplace charging only gets you so far. As ev ownership spreads from wealthier households to people living in flats or dwellings without the ability to plug in, a public network becomes vital. In America, Europe and China demand for public charging is expected to increase (see chart 3). Public chargers come in three varieties. A common kind is kerbside charging, via converted lampposts or other dedicated points, where cars might park overnight. Then there is “destination” charging, of the sort that is becoming more widely available in car parks at shopping centres, restaurants, cinemas and the like. Both kinds are level-2, with installation costs usually between $2,000 and $10,000 per point.

Fast charging, which typically adds 100-130km of range every 20 minutes, is vital on main roads for drivers making long inter-city trips and in cities for a quick emergency jolt. Commercial vehicles driving longer distances, such as taxis, need fast charging, too. But since charging firms need to recoup hefty costs of $100,000 or more per fast charger, using such facilities is pricey. To make life easier for customers, Tesla’s mapping software directs its cars on long journeys and works out the best route weaving through its dedicated “Supercharger” network. Other new ev models come with similar features.

Charging-industry insiders point out, reasonably, that both ev ownership and charging are in their infancy. Pessimism is unwarranted, they argue, based on a few short years of experience. Only one in 100 cars on the world’s roads is an ev, after all. Pat Romano of ChargePoint, one of the world’s biggest charging firms, talks of the start of “a 20-year arc”.

Fair enough. Still, future demand for charging at scale is impossible to know as yet. Expansion is coming fast, say some. Along with the momentum from electrophile governments, the opportunity to make money charging the world’s expanding fleet means that “hyperbolic growth” is on the way, says James West of Evercore isi, a bank. But exactly how many public chargers are needed for each ev on the road is “an open question”, notes Bank of America. Scott Bishop of Yunex Traffic, a division of Siemens, a German firm that makes charging hardware, hears many different answers when he asks insiders what share of chargers should be slow versus fast.

Another problem is the industry’s structure. Aakash Arora of bcg’s automotive practice calls its many complex layers the “gnarliest problem of all”. The need to co-ordinate with and get permission from many parties helps explain the slow roll-out. First, there are firms that make the chargers themselves. Then there are the operators. These might own the points, earning money from charging. Or they might collect fees for maintaining chargers operated by site-owners. Site-owners, usually businesses, other private landlords or local authorities, provide the locations for chargers and charge rent to point-owning operators. Service providers are middlemen who allow the charging to happen, with apps or cards that give access to charge points and facilitate payment.

Watt a business

Three kinds of firm are coming to rule the ev-charging roost. One is the vertically integrated car giant. Tesla has not revealed what it has spent on its “Supercharger” network, which now numbers 30,000 points worldwide. But it is probably several billion dollars. Other car firms are following, to a point. bmw, Ford, Hyundai and Daimler are partners with vw in Ionity. Its fast-charging network hopes to expand from 1,500 points to 7,000 by 2025. Electrify America, set up by vw in 2016 as part of its settlement with American regulators over its emissions-cheating scandal, now has 2,200 fast chargers in the United States. General Motors says it will spend $750m on charging. Its first move will be to install 40,000 points at dealerships.

Specialist charging businesses are also expanding. Several have gone public in the past year. None is profitable, and their revenues are tiny for now, but their market values are rising. The most richly valued (at around $7bn) is ChargePoint, which controls 44% of America’s public-charging market and is expanding in Europe. evBox, a Dutch firm, has 300,000 points worldwide, including a quarter of Europe’s public level-2 chargers and a third of fast-charging points. evgo has half the fast-charging market in America (excluding Tesla). But as Ryan Fisher of bnef notes, in the next decade charging firms will have to find business models that reliably produce profits even if governments cut subsidies.

A third category is energy firms. Fearful of losing business at petrol stations, they are developing ambitious schemes. After buying Ubitricity, a big European on-street charging firm, in February, Royal Dutch Shell, an Anglo-Dutch oil major, said in August that it planned to roll out 500,000 charging points around the world by 2025, both kerbside and fast charging. bp and Total have also been buying charging firms. Utilities are making a push, too. Wallbox, part-owned by Spain’s Iberdrola, sells chargers for homes and workplaces. The Electric Highway Coalition, made up of 17 American power companies, plans to install fast charging along inter-city routes.

Governments will act. America’s new infrastructure law sets aside $7.5bn for the installation of 500,000 public points by 2030. Mandates such as that recently announced in Britain requiring new homes, workplaces and retail sites to have charging points, adding 145,000 every year, are likely to become more common. A reason for optimism is that improvements in batteries should continue to offer ever longer ranges, and so less need for frequent charging. Newer batteries will be replenished more rapidly than today’s are, and chargers will provide current more swiftly.

Doubts about the ramp-up nevertheless persist. The numbers are still small relative to the vast scale of charging networks the world needs. More money will be required to update electricity grids to distribute power to the new source of demand. bcg forecasts that America, Europe and China, home to most of the world’s evs, will have only 6.5m public chargers between them by 2030—not enough to meet the iea’s global target of 40m. More cars will vie for each charger. Drivers may need to seek patience as well as thrills.